Emergency Expenses and American Religion

Who Can Weather a Financial Storm?

Before there was Dave Ramsey, there was Suze Orman. The OGs will know exactly what I’m talking about right now. She had a show on CNBC that ran on Saturday nights. We would watch it almost every week. I know—a young couple should have been out on Saturday night, exploring the town and meeting new people. But remember, I was a pastor during this time period, so I had to preach the next morning. So staying out late just wasn’t a good idea.

For those of you who don’t know Suze Orman, she basically did what Dave Ramsey does now—yell at people who call into the show and need advice on their financial situation. A popular segment was “Can I Afford It?“ Spoiler alert: the answer was almost always a resounding no. But I’ve always been deeply interested in how people spend their money because it’s not a situation where people can just “opt out” of the conversation. We all have to make money; we all have bills to pay. It’s just fascinating to me on all kinds of levels because it seems that no two people have the same approach to money.

The Bible Says ‘Don’t Work, Don’t Eat.’ But Does That Hold Up in the Data?

I am running a holiday special - 20% off an annual subscription to this newsletter. That brings the cost down to just $48 per year. Take advantage by clicking this button:

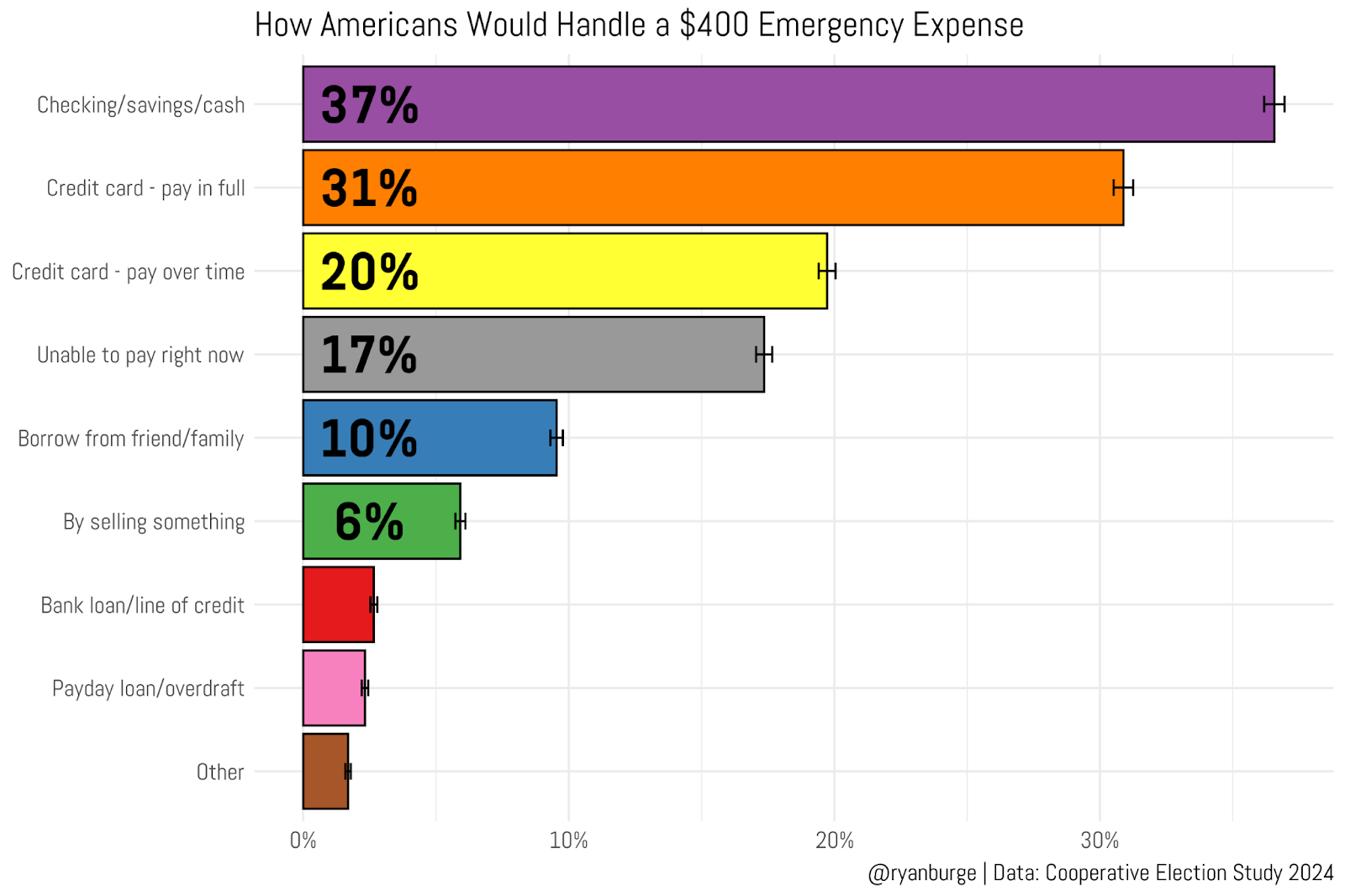

There’s this question battery in the Cooperative Election Study that asks about the respondent’s financial situation in an intriguing way: Suppose that you have an emergency expense that costs $400. Based on your current financial situation, how would you pay for this expense? Then they are given this long list of possible options, and they can check all that apply (but they do have to check at least one box). This is how respondents answered that question in the 2024 survey.

The most popular way to pay that $400 emergency expense was to just pull it out of cash on hand or a savings account. In this survey, 37% of folks would be able to find $400 without too much trouble at all. Then another 31% said that they would put the expense on their credit card and pay the bill in full when it came due. To me, that’s some pretty compelling evidence that the average American does have at least a small semblance of a financial cushion. Over two-thirds of us can just pay a small bill without going into debt.

One in five Americans would put that expense on their credit card and pay it off over time (accruing interest), 17% would just be completely unable to find $400 right now, and 10% would have to ask a family member or friend for the money. I think we can all agree that the folks who chose these last three options are in some kind of dire financial straits. A $400 expense is certainly nothing to sneeze at, but it’s not like it’s a furnace replacement that could cost ten times that amount. You can’t even buy a decent refrigerator for $400 now.

But that got me thinking: are these numbers actually good or bad? Like, is the average respondent more able to pay for a small expense today than just a couple of years ago? Lucky for us, the CES asked that question back in 2020 as well. The survey is always conducted around election time, so this was still in the throes of the COVID-19 lockdowns, and most of us had been handed a fat check from the federal government to stimulate the economy. For many, this was a time of (relative) financial abundance.

I just looked at what I consider the best and worst options here: “I would just pay the bill out of my excess funds” and “I can’t pay this bill at all.”

It’s interesting to see which religious groups seem to be doing better in 2024 compared to 2020 and which ones were doing worse. For instance, white evangelicals seem to have a deteriorating financial situation. In 2020, 45% could pay the bill with cash. That dropped to 38% in the 2024 data. That’s also true of mainline Protestants—down seven percentage points. There’s also a four-point dip among white Catholics. But what’s funny about those three groups is that the share who just flat-out can’t pay didn’t really change too much during this time period.

There are some groups that have an increase in cash on hand, though. That’s the case for non-white Catholics, Muslims, Buddhists, and Hindus. All are slightly more likely to just write the check to pay the bill in 2024 compared to 2020. But I think that stasis is pretty widespread when comparing these responses over time. No huge swings between these two surveys.

I did want to point out that the gray lines (those who just flat-out can’t find $400) are almost always flat or pointed slightly downward. I can’t find a single religious group in this data that is more likely to be in a precarious financial position in 2024 compared to 2020. That’s actually really encouraging news and counters the narrative you often hear about how the United States is in a quiet recession.

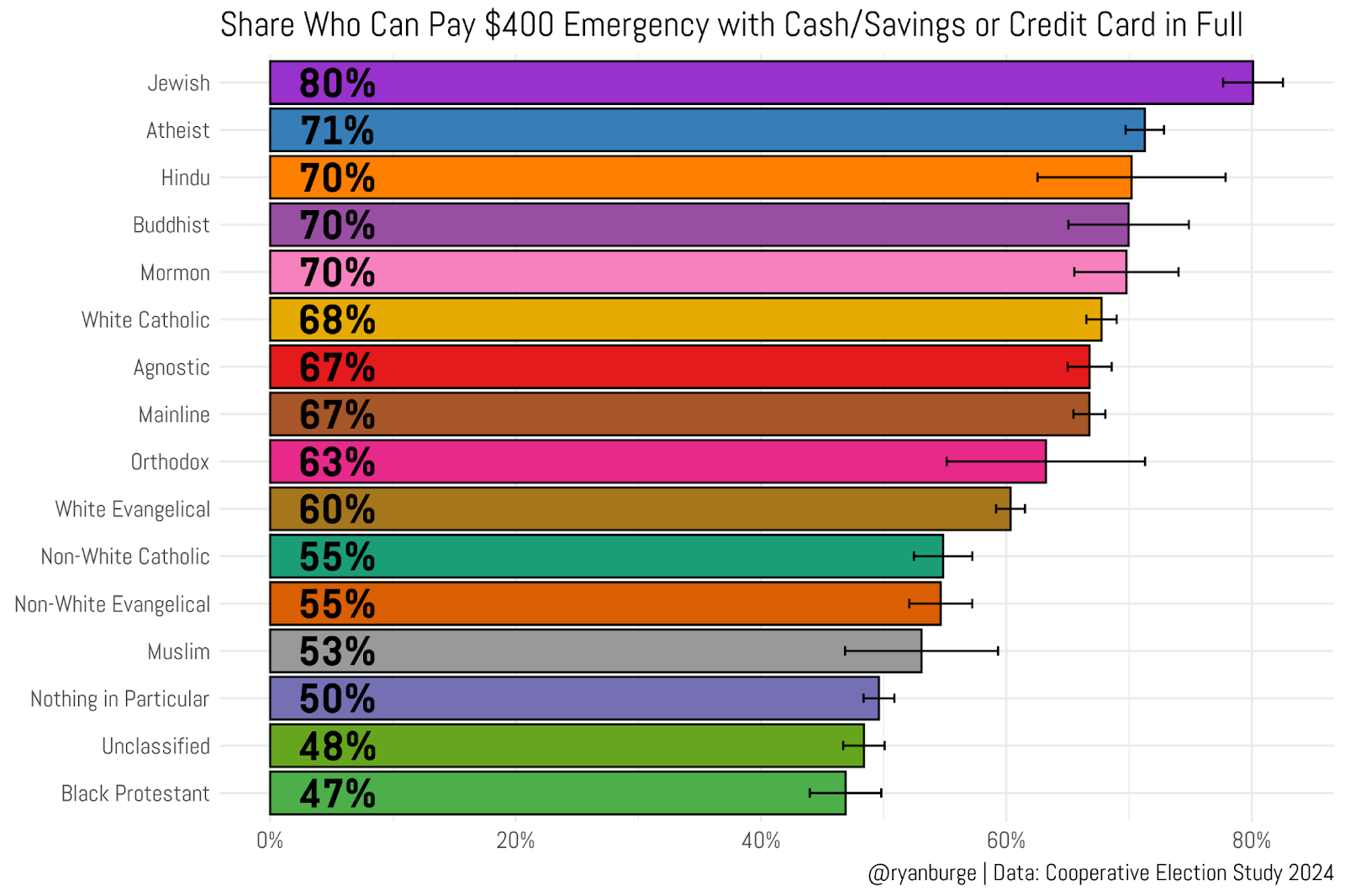

So, what share of each tradition is most able to weather a financial storm? I calculated the share of each tradition that could basically pay for a $400 expense without much trouble. They would either just write a check or put it on their credit card and pay in full at the end of the month.

Almost every group is above 50% on this metric, and many groups are far above a majority. For instance, 80% of Jews would have little problem with an unexpected expense. They are followed by atheists, Hindus, and Buddhists. Anyone who has followed my work for the last couple of years knows why these traditions show up at the top of the graph—they tend to be on the upper end of the income spectrum.

The groups at the bottom also basically follow this same pattern when it comes to having lower incomes. About half of Muslims could come up with the funds in a pinch, and the same is true for nothing-in-particulars. The only groups that fall below 50% are the unclassified and Black Protestants. But even among these groups, the percentage who could come up with the cash in a pinch is pretty robust—about 48%.

I thought I would show you the full range of data in the sortable table below. This is every tradition and every option when it comes to how they would come up with the cash. Remember that folks could select multiple options for this question. So they could say that they would both borrow some money from a family member but also pay the rest off with cash or credit, too. Feel free to point out some notable things in the comments. There are certainly a lot of data nuggets that appear here.

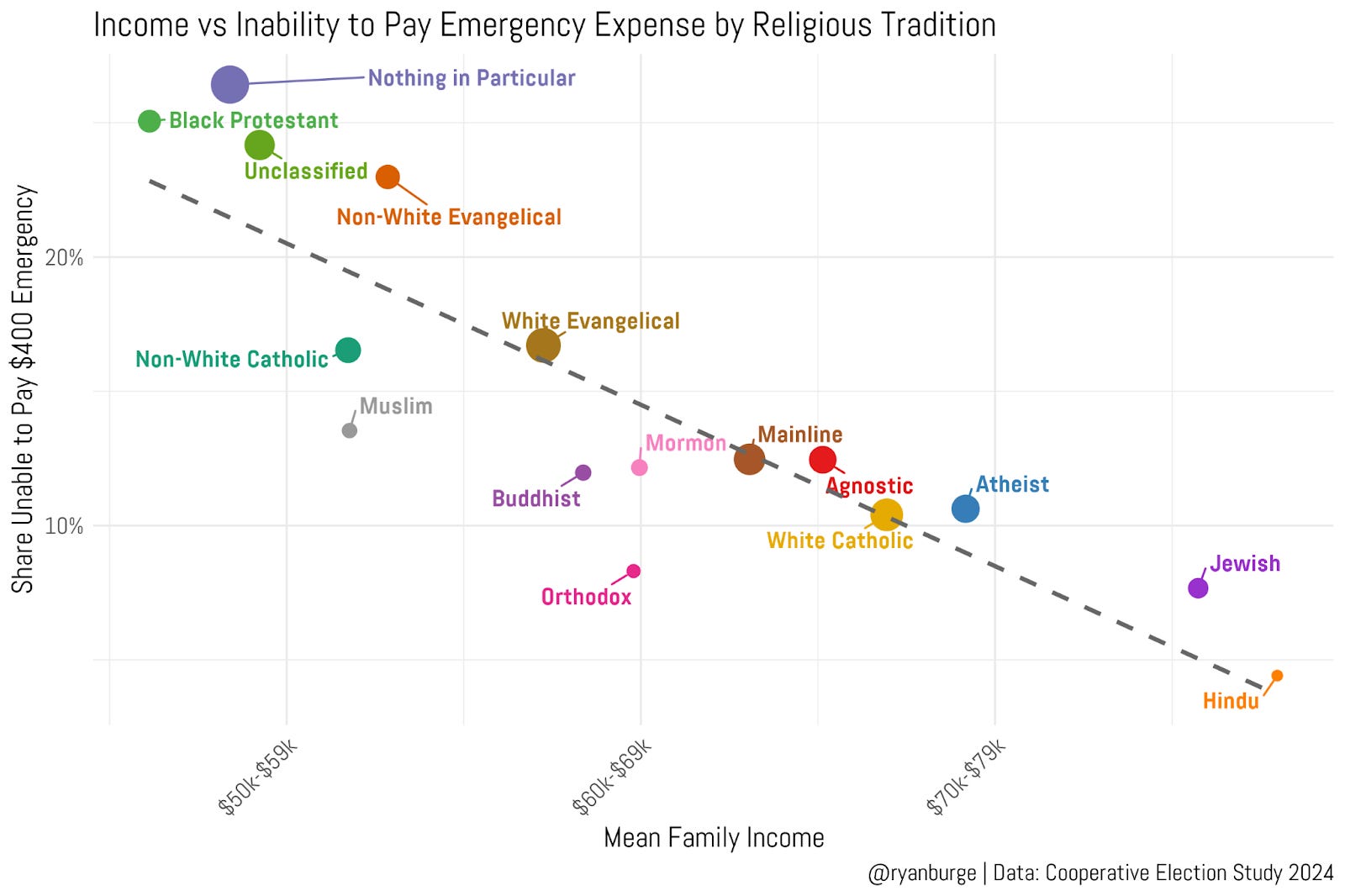

But to get back to the question of how income relates to coming up with an emergency expense, I tried to visualize what that relationship looks like in the scatterplot below. On the x-axis, I calculated the mean household income for every religious tradition. On the y-axis is the share of each group that said that they would be completely unable to pay a $400 expense if one popped up.

I don’t think anyone is going to be too surprised at seeing the downward trajectory of the trend line. Traditions with higher incomes are more likely to be able to come up with $400. You can see that with both Jews and Hindus. In each case, less than 10% couldn’t find the money in a pinch. They also both have incomes that are closer to $80K per year.

It’s pretty interesting to me how many traditions stick really close to that trend line across the range of income values. Groups like white evangelicals, white Catholics, and mainline Protestants are basically exactly where one would expect them to be based on their average income. But that’s not to say that there aren’t a few outliers that did jump out when looking at this graph.

For instance, just 8% of Orthodox Christians said that they couldn’t come up with $400. The trend line says that should be closer to 15%. So this group has more fallback plans than would be expected. That’s also the case with Muslims. They don’t have a ton of income, but only 13% of them said that they couldn’t pay that unexpected expense. The trend line predicts this figure to be closer to 19%.

So that was an interesting result to me because it got me wondering: what kind of situation does someone need to be in to not be able to come up with a few hundred dollars via any means, especially asking a friend or family member for the funds? That’s one way religion works, by the way. It becomes a kind of mutual aid society where people give a regular donation, which then flows out to help needy folks in the community. But sometimes those givers are in a financial pinch themselves and need those funds to flow back to them.

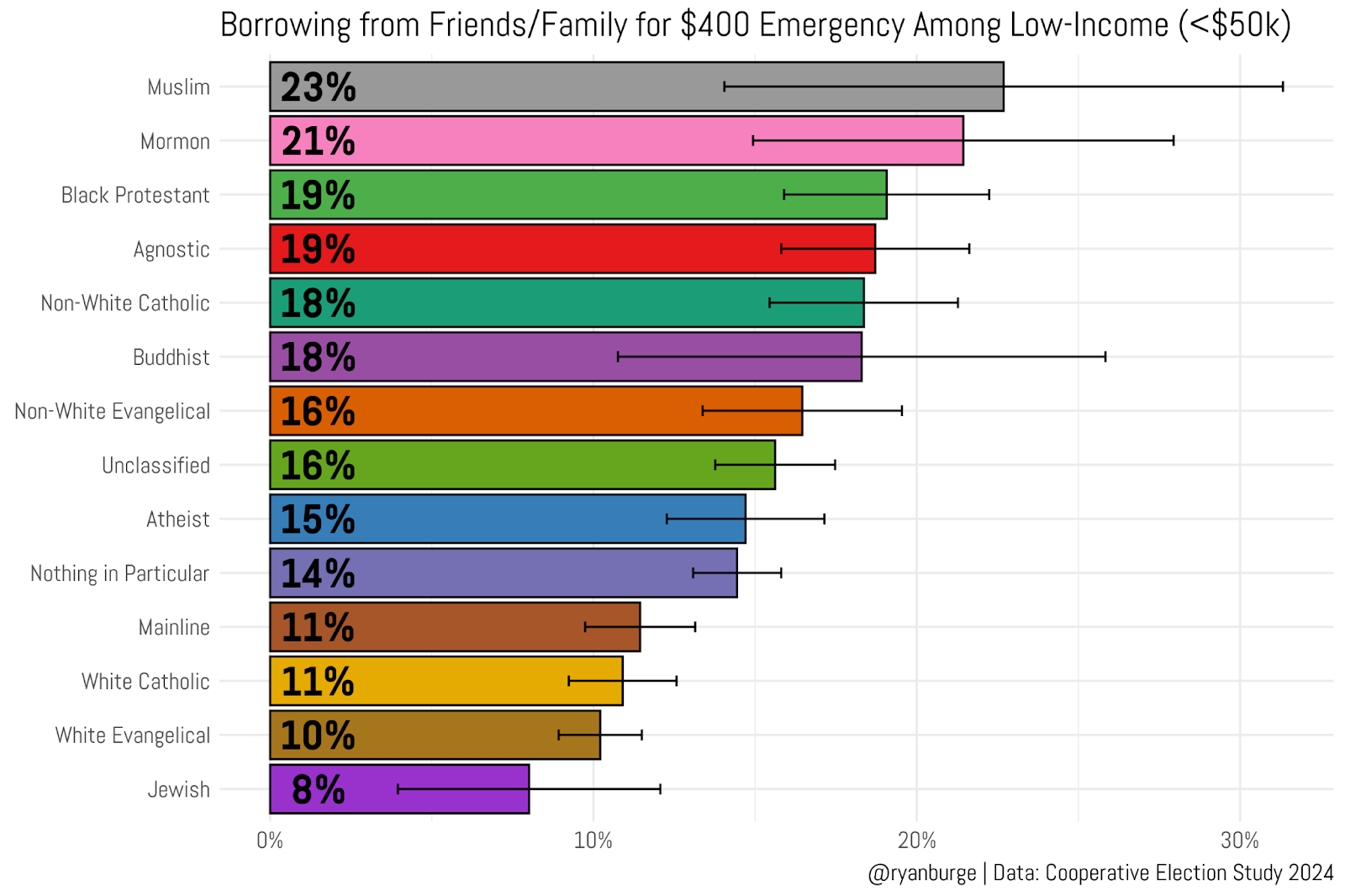

Of course, this is going to be conditioned on the income of the respondent. So I just looked at folks who made no more than $50,000 per year and calculated the share who said that they would ask a friend or family member to loan them $400 for that emergency expense.

I think this is a fascinating result because I have absolutely no idea what to make of it, honestly. I went into this thinking that religions that tend to have a stronger communal component—like Islam and Latter-day Saints—would be more able to tap into social networks to come up with the money. The data does point to this reality. Both those groups are at the top of the list, along with Black Protestants, which logically follows.

Have Clergy Made Any Wage Gains Recently?

I’ve been on the staff of three American Baptist Churches in my life. Let me tell you about the most awkward part of the process of getting hired at one of those: negotiating salary and benefits. I’m not a bashful guy by any stretch of the imagination. I mean, I talk to groups of people on a regular basis. It’s not a career path for a shrinking violet. But when it comes to the question of money, I just clam up. I’ve never been good at it.

But then at the bottom of the list, you’ve got Jews, white evangelicals, white Catholics, mainline Protestants, and then a couple of types of nones. It’s not every day where you see those disparate groups being so close together in a graph on any dimension. I mean, I can absolutely believe that white evangelicalism is near the bottom here. There’s most certainly a “personal responsibility” ethos in this tradition. That’s probably also present with mainline Protestants. But why are Jews at the bottom? Is there just an unspoken rule in Jewish culture to not ask others for money? Someone help me out in the comments.

This has been a fascinating data exercise for me. In some ways, it’s confirmed what I know about many of these groups. In other ways, it’s made me realize just how little I know about American religion—especially when it comes to money. I think there are more than enough threads to pull on in future posts about faith and money in American society.

Code for this post can be found here.

Ryan P. Burge is a professor of practice at the Danforth Center on Religion and Politics at Washington University.

Will take a crack at how we Jews extricate each other in a pinch but more from familiarity with our culture than data. We have a communal safety net called Jewish Family Services that exist in larger towns as a subsidiary of our Federation system which collects money for multiple causes, local and global. I do not know if anyone there is designated to provide short term petty cash, but individual attention to immediate problems is part of their mission.

A more interesting phenomenon is the Rabbi's Discretionary Fund. We just sold our Hametz for Passover, selecting a Rabbi as our agent to do the transaction. They get a fee of about $36 for doing this. So our Rabbi probably sold it for a hundred congregants, giving him $3600 in March. When we hold weekday services there is a collection box to which worshipers insert a dollar bill at each service. So figure about $30 a week. When the Rabbi does a special service like a wedding or a funeral, he is contractually obligated to do these. Families still pay a few hundred dollars as a donation. These funds create a Rabbi's Discretionary Fund. He does not own this money and it does not appear on the budget report at our board meetings. He has stewardship of how it is spent.

One revealing question when search committees interview candidates is to ask them how they spent their stewardship money. It is very common for them to pay utilities of older members, get Ubers to take people to medical procedures, and I assume help out with an auto repair, as well as buy materials for the congregational library or pay somebody's tuition for a continuing ed2course.

We also have dedicated funds. For Passover there is a tradition to contribute to Maot Chittim Funds which purchase Passover supplies, which have big seasonal markups, for Jews of limited means. For Purim we have an Jewish legal obligation to contribute to Matanah LEvyonim which is noted in the Megillah of Esther. It is a collection of discrtionary money, collected at the time of Megillah reading that is distributed to the Jewish poor, also in anticipation of Passover to follow. Typically people give $10-20 per familiy, so the evening will collect about $2000, all in US currency.

The Jewish standard on this has been that while we give, we tend not to give directly to panhandlers looking for bus fare or coffee. Our tradition has us choose an agent to distribute pooled funds.

Will the Jewish person at the margins get her tires replaced or her AC repaired? The community resources exist. There is also a bit of stigma to asking for it, so the requisition usually comes indirectly from somebody else familiar with the situation.

Hope the review of our traditions on this helps the readers.

I wonder how much age also factors into this? Great topic to address Ryan.